Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Tax Benefits Every Homeowner Should Know About

It’s tax season again, but being a homeowner might just make it rain at refund time. Check out the tax-deductible expenses, exemptions, and credits below. Whether you own a house, condo, or mobile home, they can save you big money when you file. Just be sure to compare your total itemized deductions against the standard deduction and see which is higher (you’ll have to choose between standard OR itemized on your return). It’s also good to know what you can’t deduct before you land in hot water with the IRS…

Mortgage Interest

A house payment is comprised of two parts: principal and interest. The principal goes toward reducing the amount you owe on your loan and is not deductible. However, the interest you pay is deductible as an itemized expense on your tax return. You can generally deduct interest on the first $750,000 of your mortgage (or $375,000 each if you’re married filing separately) if you purchased your home after December 15th 2017. Those who purchased earlier (10/14/1987 – 12/15/2017) can deduct interest paid on up to a $1m mortgage.

Property Taxes

You can deduct up to $10,000 of property taxes you paid (or $5,000 if you’re married filing separately). If you have a mortgage, the amount you paid in taxes will be included on the same annual lender statement that shows your loan interest information. If you paid the property taxes yourself but don’t have receipts, you should be able to locate the total tax amount on your county assessor’s website.

Home Improvements

Making improvements on a home can help you reduce your taxes in a few possible ways:

- If using a home equity loan or other loan secured by a home to finance home improvements, these loans will qualify for the same mortgage interest deductions as the main mortgage. Only the interest associated with the first $100,000 is deductible (and if you’ve already maxed out the interest deduction on your main mortgage, you won’t be eligible for any additional deduction for this loan).

- Tracking home improvements can help when the time comes to sell. If a home sells for more than it was purchased for, that extra money is considered taxable income. However, you are allowed to add capital improvements to the cost/tax basis of your home thereby reducing the amount of taxable income from the sale. Keep in mind that most taxpayers are exempted from paying taxes on the first $250,000 (for single filers) and $500,000 (for joint filers) of gains.

- Home improvements made to accommodate a person with a disability (yourself, your spouse, or your dependents who live with you) may be deductible as medical expenses. Examples include adding ramps, widening doorways/hallways, installing handrails or grab bars, lowering kitchen cabinets, or other modifications to provide wheelchair access.

- If you live in Washington State and apply with your county prior to construction, you may be able to get a 3-year property tax exemption for major home improvements (including an ADU or DADU) that add up to 30% of the original home’s value.

Home Office Deduction

If you run a business out of your home, you can take a deduction for the room or space used exclusively for work as your principal place of business. This includes working from a garage, as well as a typical office space. Unlike most of the other deductible expenses, you can deduct home office expenses even if you opt to take the standard deduction.

This deduction can include expenses like mortgage interest, insurance, utilities, and repairs, and is calculated based on “the percentage of your home devoted to business use,” according to the IRS.

Home Energy Tax Credits

For homeowners looking to make their primary home a little greener, either the Energy Efficient Home Improvement Credit or the Residential Energy Clean Property Credit can help offset the cost of energy efficiency improvements. Even better, these are credits, which means they directly lower your tax bill.

- Energy Efficient Home Improvement Credit: 30% of the cost for qualified high-efficiency doors, window, insulation, air conditioners, water heaters, furnaces, heat pumps, etc. Maximum credit of $1,200 (heat pumps, biomass stoves and boilers have separate max of $2,000).

- Residential Clean Energy Credit: 30% of the cost for adding qualified solar/wind/geothermal power generation, solar water heaters, fuel cells, and battery storage.

What You Can’t Deduct:

- Mortgage Insurance (this is a change as of 2022)

- Title Insurance

- Closing Costs

- Loan Origination Points

- Down Payment

- Lost Earnest Money

- Homeowner’s Dues*

- Homeowner’s/Fire Insurance*

- Utilities*

- Depreciation*

- Domestic staff or services*

*Unless it’s related to your home-office deduction—contact your tax pro to see if it’s a qualified deduction for you.

Do you have a low-income, disabled or senior homeowner in your life? Check out this article on King County property tax relief.

Psst…every homeowner’s financial situation is different, so please consult with a tax professional regarding your individual tax liability.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2024, Windermere Real Estate/Mercer Island.

Adapted from an article that originally appeared on the Windermere Blog, written by: Chad Basinger.

Property Tax Relief Programs in King County

More than 26,000 low-income seniors and disabled people in King County who qualify for a tax exemption haven’t claimed it…are you or your family member one of them?

If you are homeowner, make $58k or less per year, and are either age 61+ or retired due to disability, there is a good chance you qualify. You can even retroactively apply for the exemption for the prior 3 years!

Scroll down for details on this exemption plus 4 other property tax relief programs that King County offers.

In another county? Here is the full list of income thresholds for every county in Washington State, and here is another link to view the programs each county offers.

Senior/Disabled Property Tax Exemption

WHAT IS IT?

A reduction in King County property tax for seniors, people with disabilities, and disabled veterans.

WHO QUALIFIES?

- Seniors age 61+

or

- Those who cannot work due to a disability

or

- Veterans with service-related disabilities

YOU MUST…

- Own your home

- Have occupied it as a primary residence at least 6 months out of the year

INCOME LIMIT

- $58,423 maximum annual household income in the previous year

WAYS TO APPLY

- Click here to apply online

- Call 206-296-3920

- Ask your local senior center if they help with applications

Senior/Disabled Property Tax Deferral

WHAT IS IT?

The ability for seniors & disabled people to defer unpaid property tax/special assessments, including back taxes for as long as you’ve owned the home. Deferred taxes + any accumulated interest then become a lien on the property until it’s repaid.

WHO QUALIFIES?

- Seniors age 60+

or

- Those who cannot work due to a physical disability

YOU MUST…

- Own your home and have lived in it for more than 9 months in a calendar year

- Meet an equity requirement

INCOME LIMIT

- $67,411 maximum annual household disposable income

HOW TO APPLY

- Call 206-263-2338

MORE TAX RELIEF PROGRAMS…

Limited Income Deferral

WHAT IS IT?

The ability to defer the second installment of your property taxes/special assessments (normally due October 31st) if you are a low-income homeowner. The deferred taxes plus interest become a lien on the property until they’re repaid.

YOU MUST…

- Have owned your property for 5 years

- Be living in the home as of January 1st of the application year AND more than 9 months during that year

- Meet an equity retirement

- Have already paid the first half of your taxes (due April 30th)

INCOME LIMIT

- $57,000 maximum annual household income in the previous year

HOW TO APPLY

- Call 206-263-2338

Homeowner Improvement Exemption

WHAT IS IT?

Relief from tax increases caused by major additions or remodels.

YOU MUST…

- Own a detached single family dwelling (including mobile homes)

- File your claim for exemption with the assessor BEFORE construction is complete

HOW TO APPLY

- Call 206-263-2338

Flood & Storm Damage Property Tax Reduction

WHAT IS IT?

Tax relief for property damaged by something beyond the owner’s control. Eligible properties receive a reduction of assessed value resulting in lower property taxes. In addition, taxpayers can receive an exemption to keep taxes lower for the 3 years after they rebuild.

YOU MUST…

- Have your property on the assessment roll as of January 1st in the year it was damaged

- Have property that was destroyed, OR was in a declared disaster area and reduced in value by more than 20% as a result of the disaster

HOW TO APPLY

- Complete a Destroyed Property Claim Form and file it with King County Dept of Assessments within 3 years of the damaging event

- Call 206-263-2332 with questions

For more information on any of these programs, visit the King County Assessor’s tax relief page. You can also find info for other counties on the WA Dept of Revenue website.

© Copyright 2023, Windermere Real Estate/Mercer Island.

Thinking About Buying a Second or Vacation Home?

Here are a few tips to make sure it’s worthwhile…

These days, having your own home away from home is a compelling concept. There are many clear benefits including being able to use your home how you wish, decorate to your taste, and include your furry friends in your time away. There are also challenges to be considered as home security, maintenance, and holding expenses are nothing to ignore.

One consideration to start with is whether the home will be solely used by your family or become an income-producing vacation rental. In addition to being a lifestyle choice, this determination will impact your income taxes and insurance needs and should be made before you embark upon this journey.

There are advantages and disadvantages to both options:

Owning as a Personal Second Home

PROS

- Comfort: Returning to the same place is familiar and often more relaxing than staying in a hotel or vacation rental. It allows you to enjoy your space as you wish and include pets and hobbies in your home away from home. Proximity to your primary residence is an important factor. How long will it take to get there? You will likely visit more often if your second home takes under three hours to travel to. Choosing a location that you will enjoy for years to come is essential to making a good purchase decision.

- Convenience: The ability to keep your possessions that are used exclusively at the second home simplifies travel and packing and makes it easier to be surrounded by the things you enjoy.

- Long-term profit: While assets fluctuate in value in the short term, vacation properties are more likely to retain their value and appreciate because they are located in popular areas with a geographically limited supply. At some point you could have a nice nest egg or a property that becomes a family vacation home for future generations.

- Future retirement options: A common retirement goal is to have a place to retreat for part of the year in addition to your main residence. Whether a second home will become a full-time venue in retirement or continue to be a part-time get-away, having it established before retirement gives you options.

CONS

- Initial cost: Buying a second or vacation home is a big investment. Down payment requirements are typically higher on non-primary residences and that cash outlay can take away from other investment opportunities.

- Maintenance: Your second or vacation home will require maintenance and upkeep just like your primary residence. You’ll need to plan to tackle that yourself or hire someone else to do it for you. Let it get away from you, and you will be spending your leisure time worrying about everything that needs to get done instead of relaxing.

- Commitment: When you are paying a significant amount of money each month for a second or vacation home, you may feel that you need to constantly visit the property to justify your investment. You’ll need to ask yourself if the idea of going to the same place over and over again is appealing or a turn-off.

- Other considerations: Evaluating and mitigating your exposure to natural disaster (fire, flood, earthquake, tsunami, etc.) and liability risks (guest injury, burglary, squatting, vandalism, arson) on a home that is vacant for much of the time is an important consideration. Determine how you will keep your home safe and secure.

Owning as an Income-Producing Vacation Rental

PROS

- Income to offset expenses: A good vacation rental property generally provides a healthy rental revenue which could potentially cover mortgage payments and operating expenses. Using an online short-term rental service like Airbnb makes it convenient to manage your rental property. Their website interface makes pricing, marketing, and communication with potential guests straightforward and easy. Airbnb will also oversee the billing process for you.

- Tax considerations: You may qualify for federal tax breaks and deductions related to holding your investment property. This can help offset the expense of owning and provide investment opportunities for the future.

- Long-term profit: Like a second home, vacation properties are more likely to retain their value and appreciate over time. At some point you could have a nice nest egg or a property that becomes a family vacation home for future generations.

- Future retirement options: While there are tax considerations to converting an income-producing property into a personal use property, owning a vacation home allows you to insulate yourself against rising real estate prices and give you options for future use.

CONS

- Initial cost: Buying a vacation home as an investment property will require both a hefty down payment and initial start-up expenses to furnish and supply the home. You will need to evaluate that cash outlay with other potential investment opportunities.

- Management and maintenance: Vacation rentals can be costly to manage, both in terms of time and money. These properties may require seasonal upkeep and special maintenance considerations. You may even incur costs to maintain or monitor the property even when it’s not actively being utilized.

- Revenue fluctuations: Vacation rental properties are particularly sensitive to seasonal fluctuations and economic downturns, which could leave you financially exposed. Having a property that is attractive in multiple seasons is a definite plus.

- Short-term rental restrictions: Many state and local municipalities are seeking to reign in short-term vacation rentals, which could put a damper on potential revenue from these properties. Many now require a minimum rental period of 30 days. In contrast, there are locations that are ideal for these kinds of short-term rentals. Look into regional ordinances, do a Google search, and check out local newspapers to discover recent talk of changing or enforcing such codes.

- Other considerations: In addition to evaluating and mitigating your exposure to natural disaster and liability risks, you will want to consider other holding expenses. These might include higher renovation and repair costs due to high-use or damage. Most travelers expect the latest appliances and furnishings, so you will have to update every few years. Unfortunately, short-term renters are less likely to report any necessary repairs and guests are far less likely to treat the property with respect since there is no sense of ownership or obligation.

Final Thoughts

Regardless of your decision to use the property personally or as an investment, checking in with your CPA and financial advisor is a good first step. They can advise you of pros and cons of each approach, States that are more or less favorable to own a non-primary residence in, and whether you should establish a trust or LLC to hold the property in.

Having a savvy real estate broker help you understand the local scene, evaluate options, and provide vetted resources is essential, especially when you are looking in an area you are less familiar with.

Still have questions? Conact me for assistance with exploring a second and vacation home purchase locally, or I can refer you to a great broker in other areas you are considering.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2021 Windermere Mercer Island

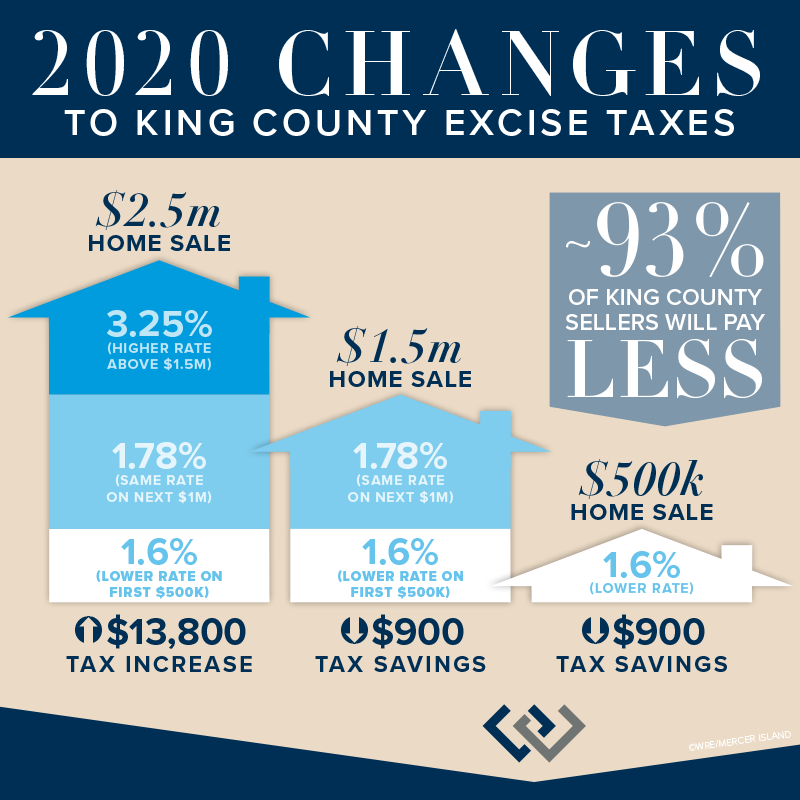

New Real Estate Excise Tax (REET) Rate (eff. 1/1/20)

Now that Washington State Senate Bill 5998 has been signed into law, our local real estate excise tax—the tax paid when you sell a property—will be getting a facelift in 2020. The flat rate of the past will make way for a new tiered system which gives owners a tax cut on the first $500,000 of home value, keeps the current tax rate on the next $1 million of value, and then increases it sharply after $1.5 million.

The good news is that taxes will go down for the vast majority (~93%) of sellers in King County. Sellers of luxury homes that fetch more than $1.56m, however, will be paying more—much, much more in the case of multi-million dollar home sales.

Wondering how the changes might impact your bottom line when it comes time to sell? Scroll down or check out our quick reference worksheet…

DETAILS & BACKGROUND

The previous flat state REET tax of 1.28% (1.78% after the 0.5% local portion is added) will be replaced on January 1, 2020, by the following rates (total REET after King County local portion is shown in parenthesis):

1.1% (1.6%) – Portion of selling price less than or equal to $500,000

1.28% (1.78%) – Portion of selling price greater than $500,000 and equal to or less than $1.5 million

2.75% (3.25%) – Portion of selling price greater than $1.5 million and equal to or less than $3 million

3.0% (3.5%) – Portion of selling price greater than $3 million

These thresholds may be adjusted again in 2022 and every four years after that using a formula for calculating value trends.

The current state real estate excise tax rate has been the same since July 1, 1989 while the local portion of the rate has been managed by each jurisdiction individually. You can find the full details in this Real Estate Excise Tax historical rates chart provided by the Department of Revenue.

The state provides a summary of the history and use of the real estate excise tax in Washington State detailing changes over the years. Currently, the bulk of the estate tax (92.3%) goes to the General Fund. Beginning January 1, 2020, and ending June 30, 2023, revenue distributions must be as follows: 1.7 percent must be deposited in the Public Works Assistance Account; 1.4 percent must be deposited in the City-County Assistance Account; 79.4 percent must be deposited in the general fund; and the remaining amount must be deposited in the Education Legacy Trust Account. Beginning July 1, 2023, and thereafter, revenue distributions to the Public Works Assistance Account increases to 5.2 percent. You can find the full law and definitions in Chapter 458-61A WAC (Washington Administrative Code).

SO WHAT’S THE BOTTOM LINE?

If you sell for $1,561,258 or less in King County, you will pay the same or less (up $900 less) in REET after 1/1/20. This is great news for most property owners in King County and across the state. Because the rate states the same on the portion of the selling price greater than $500,000 and equal to or less than $1.5 million as it currently is, all the savings comes in the portion below $500,000. This begins to whittle away as you creep above $1.5 million and into the higher tax rate of 2.75% (3.25%).

If you sell for more than that amount, you’ll be paying more–often much more. You can see from the quick reference chart below that the seller of a $2.5 million property will pay an additional $13,800, while a $5 million sale will cost an extra $55,550 and a $10 million sale a whopping $141,550 more.

Everyone will have a different take on the new tax rate, but if you have a valuable property and contributing more to the state’s coffers isn’t part of your charitable giving strategy, selling in 2019 might offer significant savings. On the other hand, selling in 2020 and beyond funds education and public works at greater levels than ever before, and that benefits everyone.

EXCISE TAX QUICK REFERENCE WORKSHEET

MERCER ISLAND

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2019, Windermere Real Estate/Mercer Island. Originally posted on Windermere Mercer Island’s “Local in Seattle” blog.

Planning ahead: how tax reform will impact your home deductions next year

While you may still be busy filing your 2017 taxes, it’s important to look ahead and be aware of how the new 2018 tax reform laws will affect next year’s return–especially if you’re a homeowner. Those who itemize will need to note some big changes in what they can and cannot deduct. Many will instead choose to use the new higher standard deduction ($12,000 for single individuals and $24,000 for joint returns) rather than itemizing their deductions.

What can you do now? Check in with your accountant for advice specific to your situation and filing status. Also, you’ll probably want to update your withholding amount to reflect the new deduction amounts. In the meantime, here is the skinny on 5 changes that may affect you if you own a home…

1. Mortgage Interest Deduction

The deduction that allows homeowners to reduce their taxable income by the amount of mortgage interest they pay has been scaled back.

- For loans taken out after 12/14/17, you can now only deduct mortgage interest paid on the first $750,000 of combined debt for primary and secondary residences (or $375,000 if married filing separately).

- Current loans of up to $1 million are grandfathered and are not subject to the new $750,000 cap if they were taken out before 12/15/17 (or if you entered into your purchase contract prior to 12/15/17 and the sale closed by 1/1/18).

- You can continue to deduct the interest on grandfathered loans even if you refinance.

2. Home Equity Loan Deduction

Under the former tax law, you were able to deduct the interest on up to $100,000 of home equity debt even if the proceeds were used for something other than buying or improving the home (for example, an equity line of credit used to pay college tuition). This is now no longer the case.

- New 2018 law eliminates the deduction for interest on home equity debt unless it’s used to buy, build, or substantially improve the home that secures the loan.

- Loans to buy second homes do not qualify for the interest deduction if they’re taken out against the equity of your primary home.

3. Deduction for Property & Sales Taxes

Tax relief for homeowners who pay property taxes has also been limited.

- Itemized deductions for property taxes, sales taxes, state income taxes, and any other local taxes will now be limited to a combined total of $10,000.

- The combined limit drops to $5,000 if married filing separately.

4. Deduction for Moving Expenses

While you used to be able to deduct some moving expenses when you moved for a new job, this deduction has been repealed for everyone except active-duty members of the armed forces.

5. Deduction for Casualty Losses

Under former law, substantial losses to your home and personal property through things like fires and robberies could be deducted from your taxable income. Under the new law, this deduction is eliminated for everything except presidential-declared natural disasters.

Want to know more?

- New Tax Brackets and Standard Deductions

- How the Reform Might Affect Home Values

- Provisions Affecting Commercial Real Estate

The above article is presented for informational purposes only and is not intended to replace professional tax advice from your accountant.

Sources:

“The Tax Cuts and Jobs Act – What it Means for Homeowners and Real Estate Professionals,” by the National Association of Realtors

“5 Homeownership Changes Coming Under New Tax Law” by NerdWallet

“Tax Reform” by the Internal Revenue Service

ABOUT WINDERMERE MERCER ISLAND

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

©2018, Windermere Real Estate/Mercer Island