Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Planning Ahead: A 12-Month Guide to Buying Your First Home

Thinking about buying a home can be daunting, especially if it’s your first time. What should be an exciting milestone can feel overwhelming without a clearly defined roadmap, and diving in headfirst without a solid plan can lead to unnecessary stress, financial surprises, and missed opportunities. However, by establishing a timeline and breaking the process down into manageable steps, you can move forward with confidence and clarity.

Here is your month-by-month guide to preparing for a successful home purchase in the following year.

12 – 10 MONTHS OUT

Know Your “Why”

Understand your motivation for buying. Are you relocating, growing your household, or ready to invest in your future? Clearly defining your “why” will help shape your search criteria and influence your budget, location, and timeline.

Set Clear Goals

Start to think about what you want in your new home. Create a list of your wants versus must-haves, including location, budget, size, and style of home. These goals will act as a compass throughout your search. Be sure to include your ideal timeline and what you hope to get out of the overall experience.

Find an Agent Who Prioritizes Your Goals and Timeline

A trusted real estate agent is more than just a facilitator; they’re a guide, negotiator, and advocate. Look for someone who understands your timeline and long-term vision and is familiar with the local market. Ask them to provide a first-time buyer’s guide or checklist to help you get started. Building this relationship early allows your agent to understand your needs and preferences in advance, setting the stage for a smoother process when you’re ready to make your move.

9 – 7 MONTHS OUT

Assess Your Finances

Take a close look at your income, debt, and spending habits. Use this time to create a monthly budget that includes future mortgage payments, utilities, insurance, taxes, and home maintenance. Many experts recommend spending no more than 28% of your gross monthly income on housing costs.

Boost Your Credit

Your credit score has a significant impact on your buying power, including your mortgage rate and loan approval. Take the next few months to pay down high-interest debt, stay current on all payments, and avoid opening new credit accounts. Check your credit report for errors and work on improving your score if needed.

Start Saving

You’ll want to have enough set aside not only for a down payment, which is typically 3% to 20% of the purchase price, but also for closing costs, moving expenses, and initial home repairs or furnishings. During this time, try to avoid nonessential major purchases and think about setting up a dedicated home savings account to stay consistent.

6 – 4 MONTHS OUT

Talk to a Financial Advisor

A financial advisor can help you align your financial goals with your homebuying plans. They can offer advice on what you can realistically afford and help identify areas to strengthen your financial readiness. You can also use tools like an online mortgage calculator to get a clearer idea of what your future monthly payments might look like.

Research Homebuyer’s Courses & Guides

Take advantage of first-time homebuyer resources, guides, and online courses. The more you know earlier on, the more confident you’ll feel.

3 – 2 MONTHS OUT

Familiarize Yourself with the Market

Start browsing homes and monitoring prices in the neighborhoods you’re interested in. Learn whether your local market is currently favoring buyers or sellers and what that could mean for your strategy.

Meet with a Lender and Get Pre-Approved

Meeting with a lender and getting pre-approved can help give you a clear picture of how much you can borrow and what price range to shop within. It also shows sellers that you’re a serious buyer when the time comes to make an offer. Your realtor can recommend trusted lenders to work with and assist you through this process.

Start Your Home Search

Now that you have your list of wants and needs and know your price range, you’re ready to start searching for your dream home. Use online property research tools to filter by location, features, and price to see what’s available in the locations you like. Narrow down your top homes and start scheduling showings and comparing listings.

1 MONTH OUT

Make an Offer

Once you find “the one,” your agent will help you craft a competitive offer, negotiate terms, and guide you through contingencies.

Get a Home Inspection

If your offer is accepted, a licensed inspector will identify any issues with the property before you finalize your purchase. Depending on what comes up, this can give you leverage to negotiate repairs or price adjustments.

THE TIME HAS COME

Closing On Your New Home

You’ve made it! During closing, you’ll sign paperwork, pay final costs, and receive the keys to your new home. Your agent and lender will walk you through the final steps to ensure everything goes smoothly.

Buying a home may seem like a big leap, but with a solid 12-month plan and the right support, it can be an extremely rewarding experience. Take it one step at a time and know that I’m here to help whenever you’re ready.

This article originally appeared on the Windermere Blog

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2026, Windermere Real Estate/Mercer Island.

Renting vs Buying: Which is Better for You?

Knowing whether it’s the right time to rent or buy depends on your buying power, what you’re looking for in a home, your local market conditions, your plans for you and your household, and the responsibilities you’re prepared to take on at your residence.

Renting gives you greater flexibility to relocate, fewer home maintenance responsibilities, and can often be more the more affordable option, depending on where you live. The extra costs associated with owning a home—interest payments, taxes, repairs—may be too much for some renters to handle.

Becoming a homeowner also has its advantages. From a financial standpoint, owning is usually better than renting in the long term—it allows you to build wealth as your property gains equity; your monthly payments are stable and actually become more affordable over time relative to your income; and some of the costs may be deductible at tax time. From a lifestyle standpoint, owning also affords you greater freedom to customize your living space.

Ultimately, the right decision depends on your situation. If you don’t plan to be living in the same place for at least five years, renting might be more logical, as it allows you more flexibility when it comes time to move again. If you’re looking to settle down for the better part of a decade or longer and can afford to buy a home, becoming a homeowner may be the better option. Here are a few additional considerations to guide your renting-versus-buying decision making process.

What are the local real estate market conditions?

Investigate the local sales and rental markets to get an idea of both typical home prices and the average monthly payment for a rental. When comparing housing costs, be sure to base your evaluation on what’s happening in your city and neighborhood, not the nationwide averages. I track these stats regularly, so feel free to contact me for an accurate update on prices in your neighborhood.

For a quarterly breakdown of local market conditions in the Seattle area, explore my Market Review page. Each report breaks down the latest figures in home sales, home prices, and days on market for regions throughout Seattle and the Eastside. They also include helpful insights and data analysis.

What can you afford?

Making the jump from renter to homeowner is often a question of affordability. Your mortgage rate will depend on your financial strength, your credit score, and other factors, so make sure to talk to a loan officer before you start looking for a home. Getting pre-approved for a mortgage will identify what you’re able to afford and helps strengthen your offer when the time comes.

To get an idea of what you can afford, try these Financial Calculators. You can estimate your monthly payment for any listing price/mortgage terms to get a well-informed picture of whether it’s the right time to buy.

Will you need to make repairs to your new home?

Buying a fixer-upper may seem like a great way to get a deal on a house, but if the money you spend on the repairs is too great, your profit could be diminished when it comes time to sell. The same is true for remodeling and improvement projects. There are various renovation financing loans available to you that can help with the costs of home repairs, though extra consultations, inspections, and appraisals are often required in the process of securing these loans. Ultimately, if you can only afford a home that demands major improvements, and you don’t have the skills to do much of the work yourself, you may be better off renting.

Can you rent part of the house you’re buying?

If you buy a house with rental-capable space (extra bedroom, mother-in-law unit, etc.), you could use the rental income to pay off your mortgage faster and contribute more to your savings. But, of course, you need to be willing to share your home with a tenant and take on the responsibilities of being a landlord or working with a professional property manager to help you with those duties. Renting out a space in your home will also require you to purchase landlord insurance on top of your existing homeowners insurance policy.

Making Your Decision to Rent or Buy

At the end of the day, the decision is up to you. Based on the conditions laid out above, it simply may not be the right time for you to buy. Fortunately, when it comes to being a homeowner, it’s not now or never. I’m happy to be your resource in gauging whether it’s the right time to buy and guiding you through the process toward homeownership. To get started, connect with me today.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2025, Windermere Real Estate/Mercer Island.

Adapted from an article that originally appeared on the Windermere blog April 11, 2022.

Buying a Fixer-Upper

For some homebuyers, a fixer-upper is their idea of a dream home. However, the process of buying a fixer-upper comes with additional responsibilities compared to properties in better condition or new construction homes. Preparing for the process comes down to creating a remodeling plan, knowing what to look for when searching for listings, and understanding what financing options are available.

Planning for a Fixer-Upper

Fixer-uppers require a future-oriented mindset. Knowing the magnitude of the projects you and your household are willing to take on will help to form your budget and your expectations as time goes on. With some basic cost analysis for any given project, you’ll have to decide whether it’s worth it to buy the materials yourself and do it DIY or hire a professional. When testing the waters for professional remodeling, get specific quotes so you can compare costs between contractors. Understand that in addition to the down payment and closing fees, the costs involved in a fixer-upper purchase have the potential to go over-budget easily. Familiarize yourself with permitting in your area to understand how to navigate any legal roadblocks in the renovation process and to better assess your timeline for your home improvement projects.

Searching For a Fixer-Upper

- Location: Whether you are purchasing a fixer-upper with plans to sell it, rent it out, or live in it, consider its location before purchasing. If you’re planning on selling or renting, location is one of the most important factors in making a return on your investment. And if you’re planning to live in your fixer-upper, keep in mind that location will be a large part of your experience in the home. If you’re looking to sell eventually, talk to your agent to identify high ROI remodeling projects that will pique buyer interest in your area.

- Scope of Renovation: If you are looking for a smaller scale renovation, look for listings that require cosmetic projects like new interior and exterior paint, fresh carpeting and flooring, appliance upgrades, and basic landscaping maintenance. More expensive and involved projects include re-roofing, replacing plumbing and sewer lines, replacing HVAC systems, and full-scale room remodels.

- Inspections: Beyond a standard home inspection, which covers components of the home like its plumbing and foundation, consider specialized inspections for pests, roof certifications, and engineering reports. This will help differentiate between the property’s minor flaws and critical problems, further informing your decision when it comes time to prepare an offer.

Financing Options

You’ll be looking at different types of mortgages when buying a fixer-upper, but keep in mind that renovation loans specifically allow buyers to finance the home and the improvements to the property together. Extra consultations, inspections, and appraisals are often required in the loan process, but they help guide the work and resulting home value. Talk with your lender about which option is best for you.

- FHA 203(k): The Federal Housing Administration’s (FHA) 203(k) loans can be used for most projects in the process of fixing up a home. In comparison to conventional mortgages, they may accept lower incomes and credit scores for qualified borrowers.

- VA renovation loan: With this loan, the home improvement costs are combined into the loan amount for the home purchase. Contractors employed in any renovations must be VA-approved and appraisers involved in the appraisal process must be VA-certified.

- HomeStyle Loan – Fannie Mae: The HomeStyle Renovation Loan can be used by buyers purchasing a fixer-upper, or by homeowners refinancing their homes to cover the improvements. This loan also allows for luxury projects, such as pools and landscaping.

- CHOICERenovation Loan – Freddie Mac: This renovation mortgage is guaranteed through Freddie Mac, allowing projects that bolster a home’s ability to withstand natural disasters or repair damage caused by a past disaster.

If you’re interested in buying a fixer-upper, connect with me – I can help you understand the process and to discuss what makes the most sense for you.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

This article originally appeared on the Windermere Blog, written by: Sandy Dodge.

When is the Best Time to Buy or Sell a Home?

Market peaks, holidays, school, oh my! Once you’ve decided that you want to sell or buy a home, the when can be tricky to tackle. Many factors contribute to optimal timing. Scroll down for the pros and cons of selling or buying in each season.

While each season has its perks and challenges, your personal circumstances will be the most important consideration. Relocation, marriage, divorce, or other life changes may mean that it makes the most sense for you to move now regardless of market factors. If you have kids in school, it may be best to wait until after the school year to make your move.

If your timing is flexible, on the other hand, you’ll also want to consider things like the condition of your property—homes that need work or have challenges with location/layout may require a hot market (or serious lack of competing inventory) in order to sell. You’ll also want to analyze the micro-market in your neighborhood, including how many other listings are currently for sale. Check out our article on timing the market for some great tips on that.

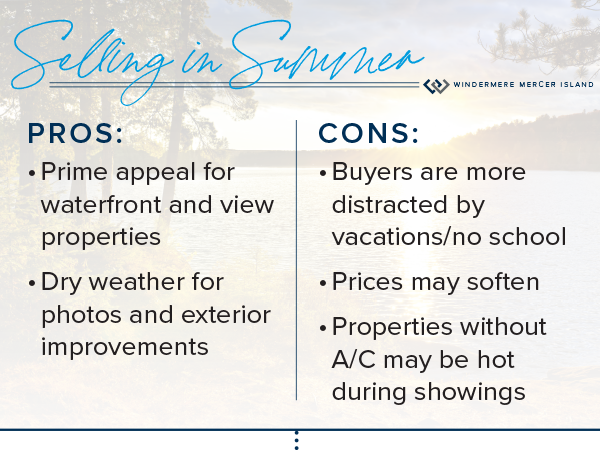

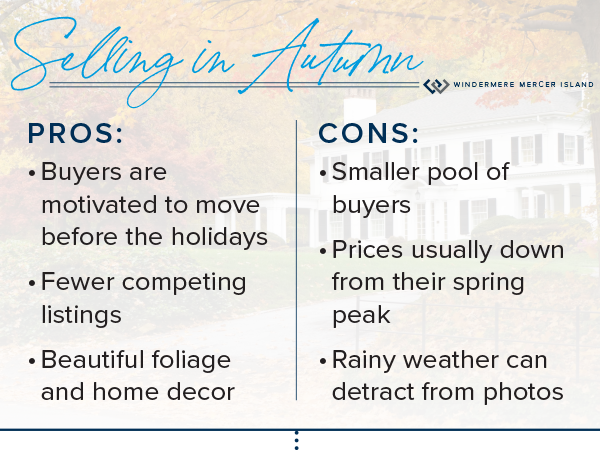

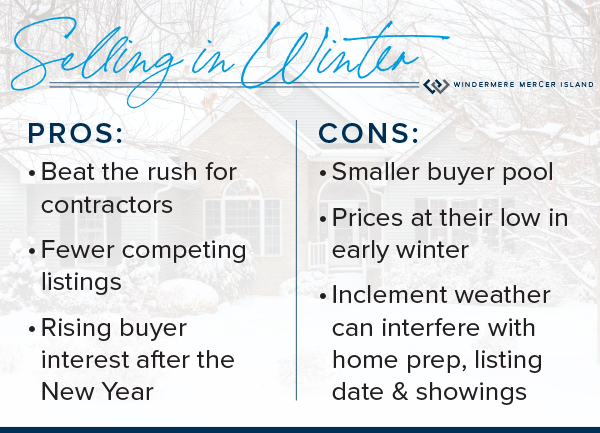

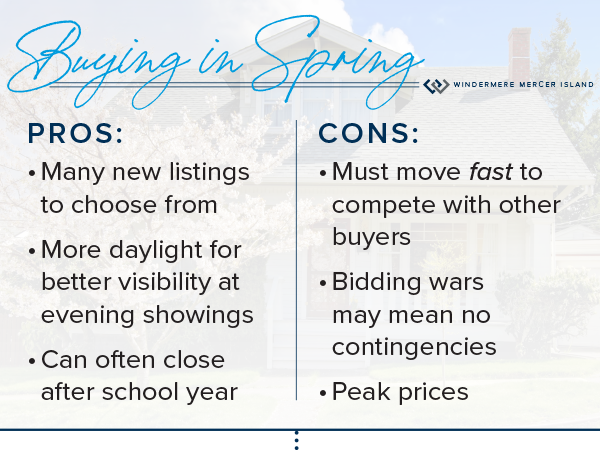

Seasonal cycles are definitely worth considering. For sellers looking to get the maximum number of eyes on your home, it’s important to avoid listing during holiday weeks or inclement weather events like snow. Buyers might find it more difficult to purchase a home at the peak of the market when homes are selling like hotcakes. Below is a chart showing typical market activity based on a five-year average of pending sales.

When my clients ask for my advice on when to sell or buy, I typically analyze all of these factors along with seasonal pricing trends. Below are some of the pros and cons I tend to see for buyers and sellers in each season…

SELLING

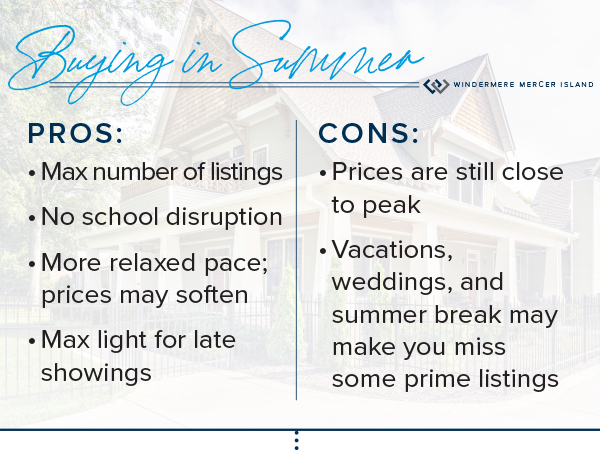

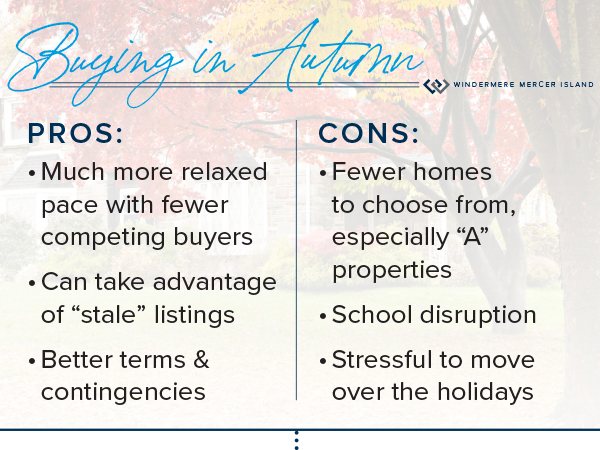

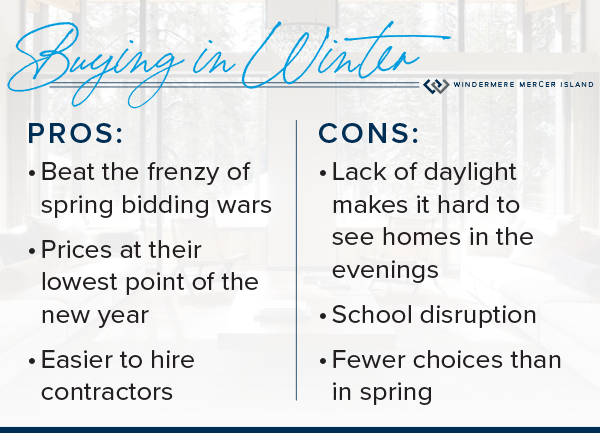

BUYING

Pssst…I know decisions like this can feel overwhelming. Reach out any time for expert advice. I’m always happy to discuss your options and help you choose the best timing for your unique property, circumstances, and micro-market…

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2023, Windermere Real Estate/Mercer Island.

Buying a Home: A Start-to-Finish Guide

You want to buy a home.

Where do you begin?

When you’re ready to buy—or maybe just ready to start seriously thinking about it—there’s a lot you can do to prepare. Here is a checklist to help you get started…

1. Determine a Price Range

Step one is finding out your budget for your new home. The best way to do that is to meet with a mortgage professional who will review your income, assets, and credit history in order to pre-approve you for a loan. Not only does getting pre-approved allow you to narrow your home search, but it also makes your offer stronger when it comes time buy. If you don’t currently have a mortgage professional, I would be happy to recommend one.

You can also use my Home Monthly Payment Calculator to experiment with different principal amounts, interest rates, down payments, taxes, and insurance to get an idea of what you can afford. Keep in mind that these calculations are meant to be estimates—interest rates change weekly and will be determined by your credit score.

2. Make a Wish List

Imagine your ideal home. How many beds/baths does it have? How big is the backyard? How close is it to the local park? Use our Wish List to guide you in your search online and with me.

3. Start Your Searching

Once you know how much you can afford and what you’re looking for in a home, it’s time to start your search. My online search tool makes it easy to search for homes, keep track of your favorites and subscribe to property alerts when a fitting listing hits the market in your area. I can also send you potential homes and take you to tour them in person once you’re ready to get serious.

4. Know What to Avoid

As you prepare to buy, knowing what not to do can often be just as helpful as knowing what to do. By understanding the pitfalls buyers can fall into, you can identify the signs of these common buying mistakes ahead of time. Check out this article on buying homes that have been flipped, too.

You’ve found the home.

What now?

Once you’ve found the home you can see yourself living in, what’s next? There are many steps to go through before you can officially call yourself a homeowner. I will guide you through this process, but in the meantime, here’s a preview of what you can expect.

1. Negotiation

When making an offer on a home, I will negotiate on your behalf in order to attain the best terms for you. This can include negotiating the price, repair costs, timelines, and contingencies.

2. Purchase & Sale Agreement (Contract)

This is the legal contract you and the seller will enter into once your offer has been accepted by the seller. It outlines the terms and conditions of the sale and is signed by both parties.

3. Inspection

Once the Purchase and Sale Agreement is signed, a home inspector is hired to examine the home’s health, safety, and major mechanical systems. If any issues arise from an inspection, you may be able to renegotiate.

In a competitive offer situation where you wish to waive your inspection contingency in order to make your offer more appealing, I may advise you to conduct a “pre-inspection”—that is, an inspection that is conducted before you put an offer in on the house.

4. Financing

After your offer is accepted, the next step is to get final loan approval. During this process the lender will decide if they’re willing to approve your mortgage based on things like your creditworthiness and the title history and appraisal of the home you want to buy.

5. Title Report

This is a report for you and your lender detailing the history of the home you’re buying to ensure there are no legal barriers to purchasing it.

6. Escrow

Escrow is an impartial third-party process in which documents and funds are deposited by buyers, sellers, and lenders to facilitate the closing of a transaction. To learn more, read this short guide to understanding escrow.

7. Closing

During this final step of the home buying process, ownership is transferred from the seller to the buyer, closing costs are paid, and several legal documents are prepared and signed, all leading to the closing date. After closing is finalized and recorded and the funds are disbursed, the home is yours!

8. Moving Day!

Check out my printable Moving Checklist as you get ready for the big day.

© Copyright 2023, Windermere Real Estate/Mercer Island.